Quarterly Results

Ashok Leyland’s Quarterly Results: Decline In Profits

Hello there, readers! L

Ashok Leyland’s Quarterly Results: Decline in Profits

Hello there, readers! Let’s look at a notable business that has advanced significantly in its sector today. A prominent player in the automotive sector who I’d like to present to you is Ashok Leyland.

Ashok Leyland, an esteemed commercial vehicle manufacturer headquartered in India, was founded in 1948. The company has a substantial local and international reach and is headquartered in Chennai.

Ashok Leyland has a long history in the commercial vehicle industry and is now known for its dependability and innovation. The company offers various products to meet transportation needs, including trucks, buses, and special application vehicles.

Quarterly Result Update

MUMBAI – On Tuesday, commercial vehicles maker Ashok Leyland reported a nearly 17% year-on-year (YoY) drop in net profit for the quarter ended March to Rs 751.41 crore, despite a rise in revenue.

Analysis on Q4 Result

- To reach Rs 11,626 crore, total operating revenue climbed by over 33% yearly.

- The company’s revenue surged by 67% to Rs 35,977 crore, while its net profit more than doubled to Rs 1,380 crore.

- Earnings before interest, taxes, depreciation, and amortisation (EBITDA), a measure of operating profit, increased to Rs 1,276 crore in the March quarter from Rs 776.1 crore a year earlier.

- Operating margins expanded 209 basis points on year to 10.97%.

- From Rs 8,240 crore in the same quarter last fiscal, total expenses, including interest costs, increased to Rs 10,597 crore this fiscal.

- On both a YoY and sequential basis, the cost of raw materials, which accounts for the majority of total expenses, increased. Input costs increased from Rs 6,430 crore one year ago to Rs 8,080.2 crore in the most recent quarter.

- The tax outlay for the quarter was Rs 373 crore as opposed to Rs 97.3 crore a year ago.

- In comparison to net debt of Rs 720 crore for the same time the year prior, the quarter saw cash generation of Rs 2,287 crore and a net cash surplus of Rs 243 crore.

Management Commentary

The CV industry is buoyant due to favorable macroeconomic factors and healthy demand from the end-user industries. This trend is expected to continue alongside growth in core sectors such as construction & mining, agriculture, increased capital outlay for infrastructure projects, and pent-up replacement demand,” said Dheeraj Hinduja, Executive Chairman, Ashok Leyland.

Despite geopolitical headwinds, the export volumes rose 2% in FY23 to 11,289 units.

The board has proposed that shareholders get a dividend of Rs 2.60 per share for the fiscal year that ended in March. If authorized at the forthcoming annual general meeting (AGM), the dividend will be paid on or before August 19, according to the Hinduja Group organization.

While the company will continue to pursue better realizations even as it expands market share, the focus will remain on bringing more profound efficiency and cost improvement, said MD & CEO Shenu Agarwal.

Shares of the company ended 0.6% down at Rs 152.20 on the National Stock Exchange on 23-05-2023.

SWOT Analysis of Ashok Leyland

- With a lengthy history and a solid reputation, this company is an established leader in the commercial vehicle sector.

- Global expansion and a strong market presence in India.

- Rise in market share on a global and domestic level.

- Adopting electric and environmentally friendly transportation allows Ashok Leyland to innovate and diversify its product line.

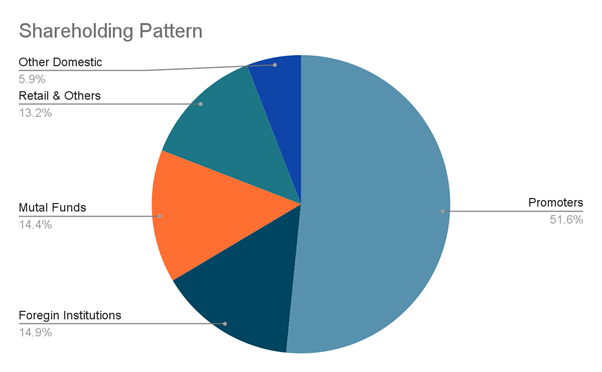

Shareholding Pattern of Ashok Leyland

Here in the above graph, we can see the major shareholders are the promoters at 51.6%, while the other domestic of 5.90%.

Here in the above graph, we can see the major shareholders are the promoters at 51.6%, while the other domestic of 5.90%.

In a nutshell

While net profit and operating margins increased, the total revenue from operations increased significantly. However, rising raw material costs were a factor in rising costs. Despite geopolitical difficulties, export volumes slightly increased. The company is focused on increasing efficiency and market share while maintaining its positive outlook on favorable macroeconomic circumstances. Ashok Leyland is still setting itself up for expansion in the automotive sector.

MTAR Technologies, a key player in precision engineering, recently disclosed its financial performance for the third quarter of FY2023, and the figures have certainly shocked the market. The company reported a significant downturn across the board, with a net profit plunge of 66.9% at Rs 10.4 crore compared to Rs 31.7 crore year-over-year (YoY), revenue dropping 26.1% to Rs 118.4 crore from Rs 160.2 crore (YoY), EBITDA falling 47.2% to Rs 23.8 crore from Rs 45.1 crore (YoY), and a margin reduction to 20.1% from 28.2% (YoY). Let’s delve deeper into these results, understand their implications, and consider the course of action for investors. Definitely, these are bad numbers and will surely impact the stock price movement tomorrow.

Unpacking MTAR Tech’s Q3 Performance

The sharp decline in MTAR’s topline to ₹118 crores from ₹167 crores in the previous quarter highlights a significant contraction in its revenue stream. Despite a decrease in material costs – from 54.4% to 48.1% – indicating improved margins, the bottom line suffered due to the fixed costs such as salaries, administration, depreciation, and finance costs outpacing the lower turnover. However, it’s noteworthy that the 9-month turnover has actually seen a 16% increase over the comparable period from the previous year.

Analyzing the Response and Future Outlook for Mtar

Investors and market watchers are keenly awaiting management’s explanation for the revenue dip and further details on order wins. It’s crucial to remember that for companies like MTAR, revenue flow can be uneven, leading to fluctuations in quarterly earnings. As a company with a 50-year legacy, MTAR’s current predicament could be a temporary setback or indicative of a deeper issue requiring strategic realignment.

Market Reaction and Investor Sentiment

During the last 3 months, MTAR’s stock experienced a downturn, dropping from Rs 2800 to Rs 1900. This decline was compounded by some level of shareholding dilution by the promoters, raising concerns about the company’s near-term prospects. Despite this, some market observers suggest that the current share price has already accounted for the disappointing results, anticipating a potential recovery. Now, we dont know how long will it take for the recovery. However, we believe that eventually MTAR will regain the all time high levels.

Guidance for Investors

In light of MTAR’s Q3 results, investors find themselves at a crossroads. Here’s a strategic approach to consider:

Stay Informed

Before making any decisions, it’s vital to understand the company’s direction and management’s strategy to address current challenges. Keep an eye out for official communications and market analyses that may shed light on MTAR’s path forward.

Long-term Perspective

For those invested in MTAR or considering it, it’s essential to evaluate the company’s fundamentals and growth prospects in the long run. Temporary setbacks can provide buying opportunities for those with a robust investment thesis and a long-term horizon.

Diversify

Diversification remains a cornerstone of risk management. Investors worried about MTAR’s performance should ensure their portfolio isn’t overly concentrated in a single stock or sector, mitigating potential losses.

Seek Professional Advice

Given the complex nature of investing in companies facing downturns, consulting with a financial advisor can provide personalized insights based on your investment goals and risk tolerance.

Mtar Tech Fundamental Analysis report below –

Conclusion

MTAR Technologies’ Q3 FY2023 results have undeniably raised eyebrows and prompted a reevaluation among its investor base. While the immediate reaction might lean towards pessimism, it’s crucial for investors to adopt a balanced view, considering both the company’s longstanding reputation and the inherent volatility of the market. As always, informed decision-making and strategic planning will be key to navigating this period of uncertainty.

A Landmark Achievement in Revenue and Profit Growth

New Delhi, India, January 16, 2024 – MapmyIndia, a leader in advanced digital maps and deep-tech products and platforms, has reported a milestone achievement in its financial performance for Q3FY24. The company’s total income surpassed Rs 100 Cr, indicating a robust growth trajectory in the Indian tech industry.

Financial Highlights of Q3FY24

A quick recap of quarterly results for MapmyIndia –

- Revenue Growth: MapmyIndia’s revenue reached an all-time high of Rs 92 Cr in Q3FY24, a significant 36% year-on-year (YoY) increase. The nine-month fiscal year (9MFY24) revenue now stands at ₹272.5 Cr.

- EBITDA Performance: EBITDA for Q3 grew by an impressive 38% YoY to ₹38.6 Cr. The 9MFY24 EBITDA increased by 32% YoY, totaling Rs 116.6 Cr, with an EBITDA margin of 43%.

- Profit After Tax (PAT): The PAT for 9MFY24 showed a 21% YoY growth, reaching ₹96.2 Cr. The PAT margin stands strong at 32%.

Strategic Wins and Operational Highlights

MapmyIndia secured a total of six major deals, each exceeding USD 10 million in total contract value (TCV), including a USD 40 million and a USD 20 million deal. The quarter also saw two significant empanelment agreements.

Advancing Technology and Market Leadership

Rakesh Verma, Chairman & Managing Director of MapmyIndia, expressed his enthusiasm about the company’s financial milestones and the consistent all-time high revenue. He emphasized the company’s strong EBITDA performance and robust PAT, reflecting MapmyIndia’s growing influence in the digital transformation space.

Rohan Verma, CEO & Executive Director, highlighted the broad-based revenue growth across various sectors and products. He noted significant achievements in auto OEM NCASE suites, consumer tech companies, enterprises, and government contracts.

About MapmyIndia & Mappls (C.E. Info Systems Ltd)

MapmyIndia, also known globally as Mappls, is India’s premier digital mapping and deep-tech company. It offers MaaS, SaaS, and PaaS, with advanced digital map data, software products, platforms, APIs, IoT, and solutions to a diverse clientele. The company has served over 2000 enterprise customers and is a pioneer in digital mapping in India, continuously evolving its AI-powered Digital Metaverse Twin of the Real World.

Impact on stock market

Trading at a very high premium of 90, MapMyIndia is not a cheap stock to purchase. Each share is trading at 2039 rupees as of today, when the market closed. Kindly consult your advisor before making any decision to purchase this stock. Its a growth company, meant for aggressive investors only.

Looking Ahead to Q4FY24

With a strong order book and anticipation of new developments, MapmyIndia is poised for an exciting Q4FY24. The company’s 360-degree marketing strategy for its consumer business has been effective, leading to increased brand awareness and product traction.

Robust Financial Performance Marks the Quarter

Mumbai, January 16, 2024 – L&T Technology Services Limited, a frontrunner in pure-play engineering services in India, has reported a significant double-digit growth in both revenue and profit for the third quarter ended December 31, 2023.

Financial Highlights of Q3FY24

- Revenue Surge: The company’s revenue stood at Rs 2,422 crore, marking a 12% year-on-year (YoY) and 2% quarter-on-quarter (QoQ) growth.

- USD Revenue Growth: USD Revenue reached $290.7 million, with an 11% YoY and 1% QoQ increase.

- Net Profit: A notable 13% YoY growth in net profit, totaling Rs 336 crore.

- EBIT Margin: The EBIT margin was reported at a healthy 17.2%.

Major Deals and Strategic Wins

The quarter witnessed L&T Technology Services securing six significant deals, each over USD 10 million in total contract value (TCV). This includes one mega-deal worth USD 40 million and another substantial deal of USD 20 million, spanning various industry segments. Additionally, the company signed two major empanelment agreements.

Advancements in New-Technology Focus Areas

Amit Chadha, CEO & Managing Director of L&T Technology Services, highlighted the company’s progress in AI, software-defined vehicles (SDV), and cybersecurity. Key achievements include:

- AI Patents: Filing 53 patents across Transportation, Medical, and Industrial Products segments.

- SDV Win: Securing a significant deal with a US OEM for next-generation automobile architecture.

- Cybersecurity Deal: A notable USD 10M+ deal win in cybersecurity.

Operational Highlights and Recognitions

- Consistent Segment Growth: Positive growth across all five segments, achieving 1% sequential growth despite seasonal softness.

- Digital Transformation Partnership: Beginning a significant relationship with bp for driving digital transformation.

- Zinnov Ratings: LTTS rated as leaders in 14 engineering domains, including Digital Engineering Services and Industry 4.0.

- Workplace Recognition: Named Most Preferred Workspace 2023 – 24 in the IT/ITES category by Marksmen Daily.

Digital Engineering Awards and Women-in-Tech Boost

The Digital Engineering Awards co-hosted by L&T Technology Services saw a record number of nominations, with women engineers’ participation doubling year-on-year.

Patent Portfolio and Human Resources

As of Q3FY24, LTTS’s patent portfolio stands at 1,249, with a significant number co-authored with customers. The employee strength was reported at 23,298. It would be interesting to see how market reacts to the quarterly results for LTTS. Investors can expect a gap up opening for sure.

About L&T Technology Services Ltd

L&T Technology Services Limited, a subsidiary of Larsen & Toubro Limited, specializes in Engineering and R&D (ER&D) services. Catering to a wide range of industries, LTTS is known for its consultancy, design, development, and testing services. With a global presence and a significant talent pool, LTTS is at the forefront of innovation and cutting-edge technology solutions.

-

Profit Making Idea1 year ago

Profit Making Idea1 year agoThe Grandfather Son (GFS) Strategy: A Technical Analysis Trading Strategy

-

Uncategorized8 months ago

Uncategorized8 months agoA BJP victory and the Stock Market: what to expect this monday

-

Technology5 months ago

Technology5 months agoInnovative Metro Ticketing Revolution in Pune by Route Mobile and Billeasy’s RCS Messaging. Stock trades flat

-

editor9 months ago

editor9 months agoHow to research for Multibagger Stocks

-

Trending12 months ago

Trending12 months agoDoes the “Tata-Apple venture” benefit Tata shares?

-

Finance World12 months ago

Finance World12 months agoHow Zomato Turned Profitable: A Landmark Achievement in the Indian Food Delivery Market

-

Market ABC8 months ago

Market ABC8 months agoSpotting an operator game: How to do it?

-

Market ABC1 year ago

Market ABC1 year agoThe Pullback Strategy: A Timeless Approach to Investment Success