news

Datamatics Global falls over 10% post Q2FY24 results. Should you buy?

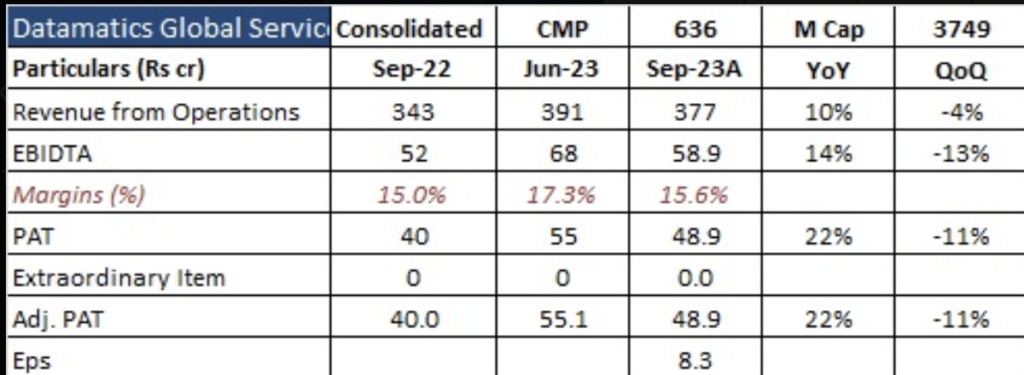

Datamatics Global closed under 600 yesterday after a moderate result. It was a shocker for the retail investors to see this potentially undervalued company go down over 14% intraday despite a double digit YoY growth in revenues and in profits. Follow along if you are wondering – “is it the right time to enter in Datamatics”?

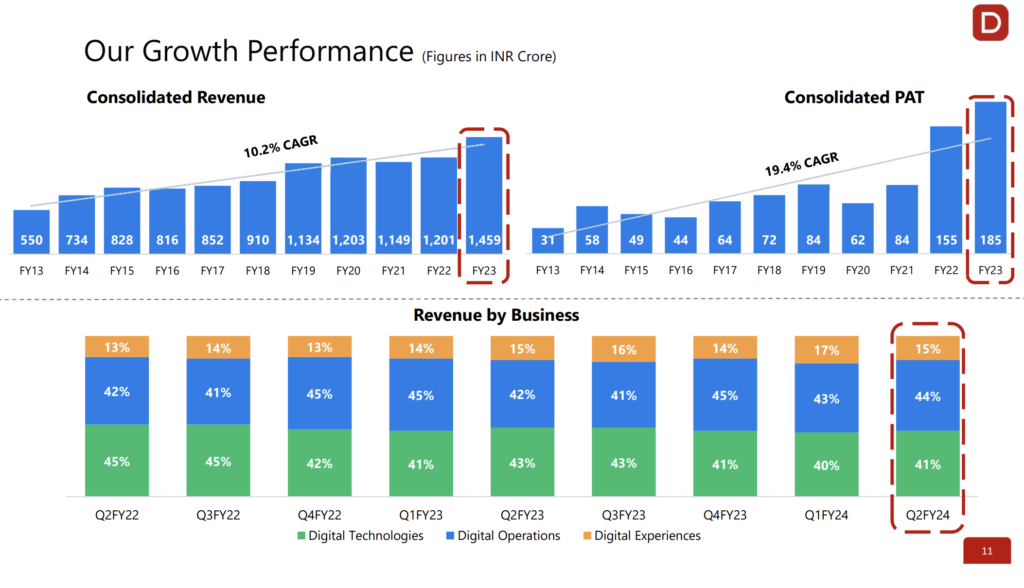

📈 Big News! Datamatics is on the upswing in Q2FY24 with an impressive 9.7% YoY increase in revenue, hitting $376.8 million! 🚀💰 Our Profit After Tax (PAT) also made a remarkable leap, soaring by 23.3% YoY to $49.3 million. 📊📉#q2fy24 #financialresults #earnings #q2results pic.twitter.com/0W7VLnx446— Datamatics (@Datamatics) November 2, 2023

What went wrong this time?

Before we jump into analysing the Q2FY23 results. Lets take a look at the possible reasons which could have been responsible behind yesterday’s fall.

- No Update on Acquisition : Datamatics Global has a market cap of around 3500 crores and has cash worth over 540 crores in its book. Despite that, Investors have been waiting on for an acquisition news from the management for over a couple of quarters now.

- Premature closure of a large project : Management did not reveal the name of the client or size of the deal. But, one thing is very clear that a major project got terminated midway this quarter to dent the revenues this time.

- Trimming down the revenue forecast : Managing director Rahul kanodia expressed difficulties to meet the earlier guided 14-15% revenue growth guidance this year. However, he did not speak much on the revised targets.

- decision making delay : Management of Datamatics informed about the decision making delays from the side of clients in these tough times regd. ramping up the project size or deal wins. This posses a challenge to precisely give an idea about whats coming!

- Revenue from Memphesis and Rapid rail deal : Huh, Its still not very clear if the revenues from both these automated ticketing projects were included in this result or not. Follow us on twitter to check on the updates as we get it.

Analysis on the results :

Datamatics Global has shown consistent growth over the past 10 years. With around 20% CAGR PAT growth for the last 10 years, Datamatics is an exceptionally great company on historical accounts.

This quarter took a hit on QoQ basis. Market was anticipating great results backed by a couple of AFC(automated fair collection) deal closures. Remember, despite the tough times in mid-cap recently, Datamatics was trading at an all time high just before the results.

We do not see any issues on YoY basis and would like to retain the initial long term opinion on Datamatics global. Check the link below to understand about the long term view on Datamatics.

What is great about the Q2 results?

Acquisition : Management quoted “We are in dialogue with some prospects and target companies. None of them have matured to the level or stage where we need to make any announcements. But yes, we are in dialogue with a few companies for application.”

Investments in AI products : Management quoted ” On the products that we talked about, which is TruCap, TruBot, iPM and things like that. We talked about an investment of INR 40 to 50 crore and that is what we are “bleeding”. They’ll be losing money. So, whatever new money comes in from revenues we would spend on sales and marketing, and we’ll maintain that INR 40-50 crore figure for the next 2 years” Increasing head-counts : In a declining IT sector, Datamatics is hiring!

Net net, we feel Datamatics still is an extremely downplayed candidate in the AI world. With a PE of just over 17 despite a PAT CAGR of over 20% for the last 10 years, its a no brainer.

Check out the official website for more details here.

Stay connected with more such guidance on your favourite companies. comment below for any company for us to cover up for you.

news

ITI Limited moves into 5G with Strategic Partnerships, stock has moved 3 times over the last year

ITI Limited, India’s pioneering Public Sector Unit (PSU) in telecom manufacturing, has taken a massive step towards improving the country’s digital landscape. By forging Memorandums of Understanding (MoU)s with Lekha Wireless, Niral Networks, and InstaICT Solution Private Limited, ITI is setting the stage for an expansive 5G ecosystem for enterprises.

A Collaborative Force in 5G Innovation

The collaboration marks a major move in ITI Limited’s journey, aligning with niche entities like Lekha Wireless, known for its Radio Access Networking prowess; Niral Networks, a beacon of Private 5G and Edge Solutions; and InstaICT Solution, experts in end-to-end network services. Together, they aim to design, deploy, and manage comprehensive Private 5G Network Solutions, heralding a new era of connectivity and digital empowerment in India.

Empowering Industries with Tailored 5G Solutions

This initiative promises to unlock new opportunities, particularly in fields that demand high-speed, reliable connectivity, such as manufacturing, energy, transportation, and more. With the hype of Digital India pushed by Narendra Modi, we feel this is just the beginning for ITI.

The Path to Digital Empowerment

Mr. Rajesh Rai, Chairman and Managing Director of ITI Limited, envisions this partnership as a cornerstone for India’s telecom technology adoption, emphasizing the transformative power of 5G in driving digital transformation across multiple sectors. The collaboration signifies more than just technological integration; it’s a step towards realizing India’s digital ambitions on a global scale.

What This Means for India’s Digital Future

The partnerships underscore a shared vision among the collaborators to accelerate India’s transition to a digitally empowered society and knowledge economy. By leveraging their combined expertise, ITI Limited and its partners are not just aiming to implement cutting-edge technology but also to catalyze sustainable growth and innovation across the nation’s industries.

Conclusion: A Leap Towards a Connected India

As ITI Limited embarks on this journey with Lekha Wireless, Niral Networks, and InstaICT Solution, the future of India’s digital infrastructure looks promising. This initiative is more than just an advancement in telecommunications; it’s a beacon of progress, innovation, and digital inclusivity for India, setting a precedent for the rest of the world to follow.

PSU stocks have seen a massive boost lately. Following the trend, the stock price for ITI has grown by over 3 times in the last 1 year. What we are worried about is the fact that the profits for the company have in-fact declined. Remember, you need to check the fundamentals of a company as well as technicals before making any investment. We see a caution from the balance sheet for ITI.

About ITI Limited: Dive deeper into ITI Limited’s legacy as India’s premier telecom company and its commitment to innovation at www.itiltd.in.

Explore Niral Networks: Learn more about Niral Networks and their revolutionary 5G solutions at https://niralnetworks.com.

Remember, the key to a successful blog post is not just to inform but to engage and inspire your readers. Ensure your post is optimized for search engines by incorporating relevant keywords throughout, such as “ITI Limited 5G partnerships,” “digital transformation in India,” and “private 5G network solutions,” without compromising readability and engagement.

Hinduja Global Solutions (HGS), known for its digital transformation and business process management services, recently showcased impressive growth in the third quarter of FY2024. Despite the tough global economic climate, HGS has shown resilience and agility, recording a significant upswing in both revenue and EBITDA. Let’s dive into the details of HGS’s performance and its forward strides in the digital domain.

Impressive Growth Metrics

Hinduja Global announced a 7.6% year-on-year increase in operating revenue, reaching Rs. 1,203.7 crore for Q3 FY2024. The operating EBITDA saw a staggering 39.9% growth compared to the same period last year, amounting to Rs. 115.1 crore. This growth trajectory isn’t just limited to a single quarter; the first nine months of FY2024 saw operating revenue at Rs. 3,517 crore and operating EBITDA climbing 39.3% year-on-year to Rs. 289.5 crore.

Strategic Client Acquisitions and Innovations

HGS didn’t just stop at financial growth; the company also expanded its clientele significantly. With 12 new logos added for digital-enabled customer experience (CX) solutions and eight for HRO/Payroll Processing, HGS is broadening its horizon. The introduction of NetX, a collaborative innovation between the digital teams of the BPM and Digital Media businesses, marks a pivotal step towards revolutionizing digital networking.

Digital Media Business Leap

The Digital Media division, under the brand CelerityX, is making waves in broadband and digital television growth. The division ended Q3 with a whopping 5.75 million connected homes across India. Furthermore, CelerityX is rolling out cutting-edge solutions, like NetX, to transform the digital landscape for enterprises across various sectors.

The Road Ahead

The journey doesn’t end here for HGS. The company is setting sights on further growth and market penetration. With aggressive investments in technology and talent, particularly in areas like Cloud, analytics, and AI, HGS is gearing up to meet the increasing market demand for complex, technology-driven solutions.

Conclusion: A Steady Climb to Success

HGS’s performance in Q3 FY2024 is a testament to its strategic planning, innovative solutions, and relentless pursuit of excellence. As HGS continues to evolve and adapt to the changing market dynamics, it is well-positioned to not only meet but exceed its growth targets, ensuring a brighter, technology-driven future.

This narrative of growth and innovation underscores HGS’s commitment to delivering exceptional value to its clients while paving the way for a sustainable and digital-first business ecosystem. Check more latest Quarterly results on Tradealone.

Yatra Online Limited, India’s leading name in corporate travel services and a dominant player among the Online Travel Agencies (OTAs), just announced its financial outcomes for Q3 of the fiscal year 2023-24, marking significant jump in revenue growth and operational achievements. Moreover, we see an increasing trend of online bookings in India, this could be a big boost for yatra in longterm.

A look into Q3-FY24 Financial Performance

The third quarter has been fruitful for Yatra, with notable financial highlights:

- Revenue Growth: The operations revenue saw a jump to INR 1,103Mn, marking an impressive 23% growth Year-over-Year (YoY).

- Net Profit Leap: Net profit witnessed a substantial rise of 119% YoY, with a diluted EPS of INR 0.07.

- Debt Reduction: The company’s gross debt was significantly reduced by 51% on a Quarter-over-Quarter (QoQ) basis.

Despite facing challenges in the corporate business segment due to subdued business travel spends, especially from IT/ITES clients, Yatra’s operational highlights paint a promising picture of resilience and growth.

Operational Highlights: A Testament to Strategic Excellence

- Dominating Air Passenger Growth: Yatra’s domestic air passenger segment outperformed, registering a 26% YoY growth, nearly tripling the industry’s 9% benchmark.

- Gross Bookings Increase: An 18% YoY growth in gross bookings, amounting to INR 18,605 Mn, underscores Yatra’s robust market strategies.

- Expanding Corporate Clientele: The addition of 26 new corporate accounts with a potential annual billing of INR 2,237 Million highlights Yatra’s strong foothold in the corporate travel sector.

Management Insights: Steering Towards a Brighter Horizon

Dhruv Shringi, Yatra’s Whole Time Director & CEO, shared his enthusiasm over the quarter’s performance. Highlighting the air passenger segment’s robust growth and the successful onboarding of new corporate clients, Shringi’s comments reflect Yatra’s unwavering commitment to market leadership and customer value enhancement. The introduction of the Yatra Prime membership initiative for Indian shareholders further exemplifies this commitment.

Furthermore, this is second good quarter in a row for yatra. checkout our previous coverage here.

Looking Ahead: Embracing Growth and Innovation

As Yatra continues to navigate the dynamic travel industry landscape, its focus on capturing growth opportunities and enhancing travel experiences for its customers remains on top. With a strong foundation , we believe Yatra will continue to grow and capture more market share.

Despite this good growth, the stock price is down by over 30% in the last year. However, we believe that as company starts to post consistent results, stock price will appreciate eventually.

Stay tuned for further updates as Yatra Online Limited continues to redefine travel experiences and value creation for its customers and shareholders alike.

Disclaimer: This blog post is for informational purposes only and is based on the Q3 FY24 earnings release by Yatra Online Limited. Readers are advised to do their own research or consult a financial advisor before making any investment decisions.

-

Profit Making Idea1 year ago

Profit Making Idea1 year agoThe Grandfather Son (GFS) Strategy: A Technical Analysis Trading Strategy

-

Uncategorized8 months ago

Uncategorized8 months agoA BJP victory and the Stock Market: what to expect this monday

-

Technology5 months ago

Technology5 months agoInnovative Metro Ticketing Revolution in Pune by Route Mobile and Billeasy’s RCS Messaging. Stock trades flat

-

editor9 months ago

editor9 months agoHow to research for Multibagger Stocks

-

Trending12 months ago

Trending12 months agoDoes the “Tata-Apple venture” benefit Tata shares?

-

Finance World12 months ago

Finance World12 months agoHow Zomato Turned Profitable: A Landmark Achievement in the Indian Food Delivery Market

-

Market ABC8 months ago

Market ABC8 months agoSpotting an operator game: How to do it?

-

Market ABC1 year ago

Market ABC1 year agoThe Pullback Strategy: A Timeless Approach to Investment Success