Profit Making Idea

How to use PE ratio to evaluate stocks?

Price to earnings ratio stands for price to earnings ratio of a company. Before we talk about how to read PE ratio before evaluating a stock, lets learn more about what does PE ratio mean?

Investors consider several metrics and indicators to evaluate stocks before investing. These help investors to make fruitful investing decisions. One such metric is Price to earnings ratio (PE ratio).

Let’s learn more about the PE ratio and how it is used by investors to evaluate stocks.

What is the PE ratio? How to calculate the PE ratio?

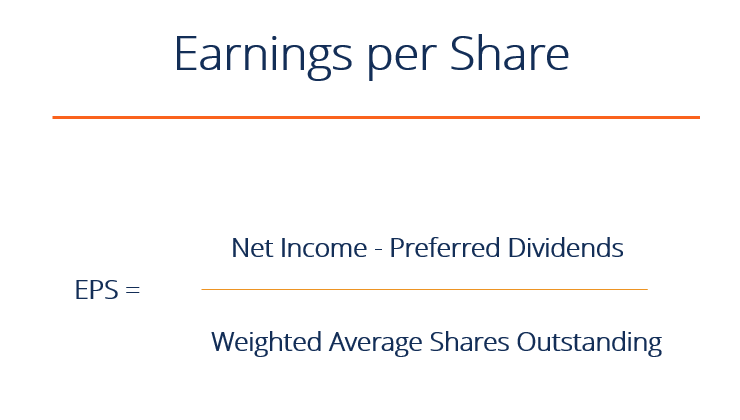

Price earnings ratio compares the last traded price of the stock to earnings per share (EPS). It gives a quantitative value of how much investors are willing to pay for each rupee of the company’s earnings.

Price to earnings ratio = Last traded price of stock/ earnings per share (EPS)

Earnings per share= Profit before tax (PAT) /number of shares

For example, A company’s profit after tax (PAT) is Rs 1, 00,000 and the number of shares is 1,000. So, its EPS comes out to be 100. Now, the last traded price of the stock of the company stands at Rs 500, so, its PE finally comes out to 5.

EPS = 1, 00,000/1,000 = 100

PE ratio = 500/ 100 = 5:1

This 5:1 ratio indicates that investors are ready to pay 5 times the earnings i.e. for Rs 1 they are willing to pay Rs 5.

How to interpret?

Investors interpret the PE ratio to evaluate whether the stock is overvalued or undervalued. Ideally, if the company’s PE ratio is low, it indicates that the company’s share is cheap similarly; if the company’s PE is high it indicates that the company’s share is expensive. Although it doesn’t give any signal to invest in the company.

The PE ratio is determined as cheap or expensive after comparing it with its peers.

For example:

| Company | Earnings (EPS) | Share price | PE RATIO |

| Datamatics | 100 | 1000 | 10 |

| Infosys | 100 | 5000 | 50 |

| Tata Power | 100 | 8000 | 80 |

In the example above, the PE of Datamatics is more, which indicates that its share price is more expensive (overvalued) than that of Infosys. If we compare Tata Power PE to Infosys having PE 50, the share price of Infosys will seem cheaper in that comparison.

A higher PE suggests that the stock is overvalued and investors are paying a premium and they have high expectations for its growth. Similarly, a lower PE suggests that the stock is undervalued and investors have low expectations for its future profits.

Factors affecting price to earnings ratio of a company –

Growth prospects:

Different sectors have different PE ratios because of varying growth potential and risks involved. Companies such as Bajaj Auto Limited, Maruti Suzuki India Limited, Shree Cement Limited, and Olectra Greentech don’t have stable earnings, industry volatility, or legal or regulatory challenges and hence have lesser PE. Similarly, companies having stable earnings and reliability attract higher PE, such as Datamatics Ltd.

Debt factor for a company:

Companies having less debt attract higher PE ratios because investors may be more interested in investing in companies having less financial cost.

Return on Investment:

ROE of the company directly influences the PE of the company. ROE measures a company’s profitability by evaluating the return it generates on the shareholders’ equity. Higher returns attract higher PE.

In conclusion, price to earnings ratio is a tool for investors to evaluate stocks and invest wisely. PE ratio should be compared with other peers and always be used in conjunction with other metrics and indicators.

Find out companies with lower Price to earnings ratio below

Hey investors! Let’s talk about Infosys and its recent ups and downs. Despite some not-so-great results, their ADR (American Depositary Receipt) is up by 5%. It’s a bit of a head-scratcher, right? So, what should you, as an Indian investor, do in this situation? Let’s break it down.

The Latest with Infosys

- ADR Up by 5%: Even though the results weren’t strong, Infosys’ ADR went up. It seems like the market had already anticipated this, and maybe some short sellers got caught off-guard.

- Q3 Results: The revenue barely budged, and net profit actually fell by 7% compared to last year. Not the best news, honestly.

- In Semi Acquisition: A big move by Infosys, acquiring In Semi, a big name in semiconductor design and embedded services. This could be a game-changer in the long run.

Analyzing the Numbers

- Profit and Revenue: The net profit is down, and revenue growth is almost flat. High interest costs are partly to blame here.

- New Deals Dropped: New deal signings took a nosedive from $7.7 billion to $3.2 billion. That’s a big drop.

- Attrition Rate: Good news here – it’s down to 12.9%. Less employee turnover is always a positive.

- Guidance for FY24: Infosys expects revenue growth of 1.5%-2.0% and an operating margin of 20%-22%.

What’s the Deal with Insemi?

Insemi’s acquisition is quite a highlight. They’re leaders in the semiconductor design space. This market is booming and expected to hit $800 billion by 2028. With Insemi, Infosys could become a significant player in this field.

The Mixed Bag

- Sector and Geographic Performance: Financial services and North America are still not performing well, but there’s some rebound in Europe.

- Cash Flow: Infosys has a healthy free cash flow, which is a good sign for its financial health.

So, What Should You Do?

- Understand the Big Picture: Look beyond just this quarter. Infosys is making moves that could pay off in the long run, especially with the Insemi acquisition.

- Diversification: Don’t put all your eggs in one basket. It’s crucial to have a diversified portfolio.

- Stay Updated: Keep an eye on how Infosys performs in the coming quarters, especially in their new ventures and market segments.

- Risk Assessment: Be aware of the risks involved. Infosys is facing some challenges, and you need to decide if you’re comfortable with that level of risk.

Final Thoughts

Infosys’ results were a mixed bag, and the stock’s reaction was a bit surprising. As an investor, it’s essential to stay informed and make decisions based on a comprehensive understanding of the company’s performance and potential. Keep watching the market and adjust your strategy as needed. Remember, investing is a marathon, not a sprint!

Since we talked about this IT giant Infosys, Lets explore some AI based companies as well.

Edelweiss Financial Services Limited has announced a public issue of Secured Redeemable Non-Convertible Debentures (NCDs) worth Rs 2,500 million, offering an effective yield of up to 10.46% per annum. With credit ratings from CRISIL A+/Stable and ICRA A+, these NCDs provide a safe investment avenue.

Issue Details and Tenures

The NCDs offer ten series with fixed coupons and tenure options of 24, 36, 60, and 120 months, presenting diverse interest payment frequencies. The effective annual yield for these NCDs ranges from 8.94% to 10.46% per annum, catering to different investment preferences.

Offering Timeline and Utilization of Funds

Scheduled to open on January 9, 2024, and close on January 22, 2024, at least 75% of the raised funds will be directed towards repaying/prepaying existing borrowings, ensuring financial stability. The remainder will support general corporate purposes, aligning with SEBI NCS Regulations.

Investor Incentives and Ratings

Investors holding debentures/bonds from the company or related entities may enjoy an additional incentive of up to 0.20% p.a. These NCDs carry ratings of CRISIL A+/Stable and ICRA A+, indicating stability despite negative implications.

Lead Managers and Listing

Trust Investment Advisors Private Limited and Nuvama Wealth Management Limited are the lead managers for this NCD issue, aiming to list the NCDs on BSE Limited. This listing will provide liquidity and ease of trading for investors.

About Edelweiss Financial Services Limited

Edelweiss Financial Services Limited, established in 1995, operates in investment banking and holds a prominent position in the financial sector. Starting as an investment banking firm, it later expanded its operations, reflecting strong credentials in financial services.

Edelweiss Financial Services Limited has unveiled a lucrative investment opportunity through its NCD issue, promising secured returns and prudent utilization of funds. As the issue opens for subscription, it’s an opportune moment for investors seeking stable yet high-yield investment avenues. With a diversified range of tenure options and regular interest payments, this offering aligns with different investor preferences. The company’s extensive experience in the financial sector adds credibility to this investment opportunity, promising reliable returns.

Key Takeaways

- Lucrative Investment Avenue

- Secured, High-Yield Returns

- Diverse Tenure Options

- Prudent Utilization of Funds

This blog introduces an investment opportunity provided by Edelweiss Financial Services Limited, shedding light on its NCD issue’s specifics and the company’s background. With its high yield and secure nature, this offering presents a compelling choice for investors seeking stable returns. Learn more about financial goal planning.

Allcargo Terminals Limited has recently hit the headlines with its stock price soaring to a 20% upper circuit. This remarkable surge raises an intriguing question: can we expect this rally to continue? Let’s dive into the company’s recent performance and sector trends to uncover insights. The upper circuit today was followed by a trendline breakout, shared by a user on twitter a few days ago.

The Catalyst Behind the Surge

Allcargo Terminals’ stock hitting the upper circuit is not just a random spike; it’s backed by solid performance and strategic moves. The company’s recent financial results for Q2FY24 show a robust 13% year-on-year increase in Container Freight Station (CFS) volumes, outpacing industry growth. But what does this mean for the stock’s future trajectory?

Analyzing Q2FY24 Performance

In Q2FY24, Allcargo Terminals demonstrated strong sequential improvement. The company not only witnessed a 6% quarter-on-quarter increase in CFS volumes but also reported revenue growth of 3% and a notable 12% increase in EBITDA. These figures indicate a positive momentum, which could be a key factor in driving the stock’s rally.

Digital Initiatives and Customer Experience

A significant aspect of Allcargo Terminals’ strategy is its focus on digital initiatives aimed at enhancing customer experience. This progressive approach is gaining traction, potentially contributing to the ongoing volume momentum. Such forward-thinking strategies are crucial in determining whether the rally has the legs to continue.

Leadership and Financial Health

The induction of Mr. Pritam Vartak as CFO marks a strategic strengthening of the leadership team, potentially boosting investor confidence. Furthermore, the company’s robust balance sheet and net debt-free status provide a solid foundation for sustainable growth, which could be pivotal in maintaining the rally.

Allcargo Terminals in the Wider Logistics Sector

Allcargo Terminals, with its extensive network and digital prowess, is well-positioned in the logistics sector. As the industry navigates through a period of transformation, ATL’s innovative approach and strategic expansions could play a crucial role in sustaining its market rally.

The Road Ahead: Predicting the Rally’s Course

While Allcargo Terminals’ recent performance is impressive, predicting the stock market is always a complex endeavor. Factors such as broader market trends, economic conditions, and company-specific developments will influence the stock’s trajectory.

In conclusion, Allcargo Terminals Limited’s recent upper circuit hit reflects its strong performance and strategic initiatives. While the current indicators are positive, the sustainability of the rally will depend on continued performance excellence and favorable market conditions. What’s your take on Allcargo Terminals’ future in the stock market? Let’s engage in a discussion about the exciting possibilities ahead for this dynamic company! 🚀💹📈

We like Adani ports as well in the shipment and cargo field. Keep following us for more such technical analysis.

-

Profit Making Idea1 year ago

Profit Making Idea1 year agoThe Grandfather Son (GFS) Strategy: A Technical Analysis Trading Strategy

-

Uncategorized8 months ago

Uncategorized8 months agoA BJP victory and the Stock Market: what to expect this monday

-

Technology5 months ago

Technology5 months agoInnovative Metro Ticketing Revolution in Pune by Route Mobile and Billeasy’s RCS Messaging. Stock trades flat

-

editor9 months ago

editor9 months agoHow to research for Multibagger Stocks

-

Trending12 months ago

Trending12 months agoDoes the “Tata-Apple venture” benefit Tata shares?

-

Finance World12 months ago

Finance World12 months agoHow Zomato Turned Profitable: A Landmark Achievement in the Indian Food Delivery Market

-

Market ABC8 months ago

Market ABC8 months agoSpotting an operator game: How to do it?

-

Market ABC1 year ago

Market ABC1 year agoThe Pullback Strategy: A Timeless Approach to Investment Success